What is a debt investment?

To define a debt investment, we must first clarify what we mean by an alternative investment. An alternative investment is an investment that falls outside of the traditional investments of cash, stocks and bonds.

However, the term ‘alternative’ in this context is becoming less relevant as investments such as property are becoming increasingly popular, with many different ways to invest in property itself.

One such way to invest in property that is seeing a significant rise in activity in recent years is debt investment.

Broadly speaking, a debt investment is a loan that is given from an investor with the expectation to receive a return on their initial investment plus a fixed rate of interest. Loan notes and peer to peer (P2P) investing have been the major investments to see this rise over the past decade or so.

What is making debt investment so attractive though? Why are investors being drawn into this investment over other types of investing?

The current portfolio of UK investors

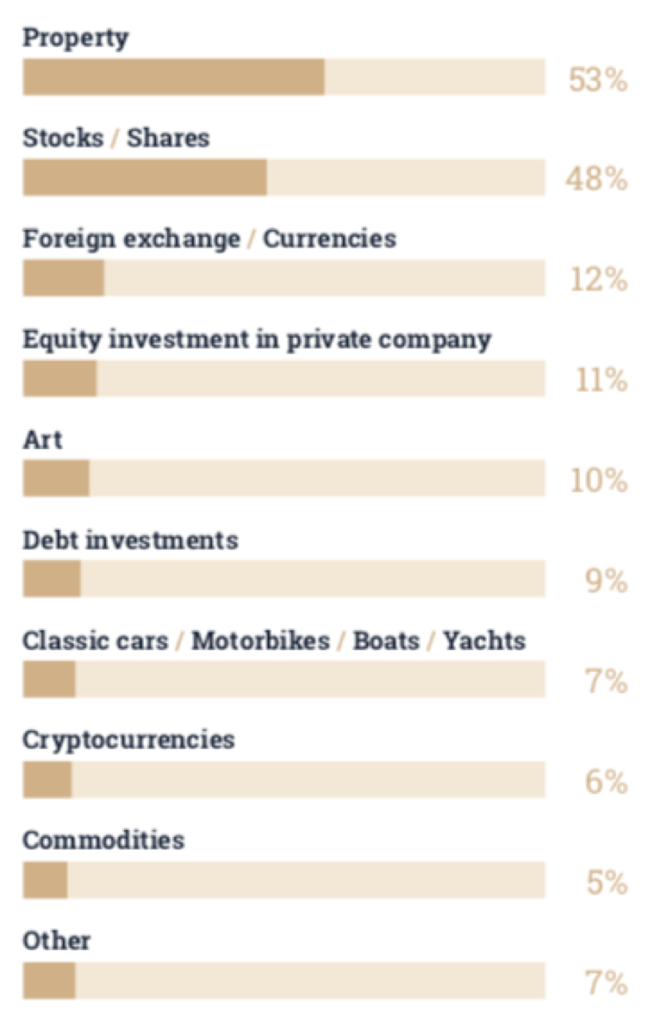

To understand the significance of debt investment in the current market, we asked over 950 verified UK investors where they currently hold investments, you can see the results of this below.

UK Investor portfolio, FJP Investment

The above findings highlight that property is by no means an ‘alternative investment’, with over 50% of investors holding a property investment. This will not come as a huge surprise to most; UK investors have long had an interest in the security of ‘brick and mortar’ investments.

9% of investors surveyed held a debt investment of some kind, whether P2P or loan note. Whilst this figure in itself is not hugely substantial, the trends emerging with investors in this type of investment is.

Debt investment growing in popularity

There are some interesting findings when you look at the trends in investors behaviour towards the investment, the most significant being the age demographic of investors. Four times as many investors under the age of 35 held an investment (16%) when compared to investors over the age of 55 (4%).

When you compare this with the number of investors in property, this result paints an even clearer picture. 65% of over 55’s held a property investment compared to just 32% between the ages of 18 and 34.

This would suggest that we are seeing a shift in investment from traditional property investments to the higher yielding debt investment through the next generation of investors.

You could argue that the lower entry point for a debt investment could be attracting those with less disposable income, and we may continue to see these demographics remain unchanged going forward, ultimately only time will tell on this front.

There is hesitancy in the market

There is some hesitancy when it comes to investing in this alternative asset. Although there is real interest, many have concerns about investing in the market.

Although many investors value the pre-defined, structured returns that you can receive with a debt investment, concerns about the repayment not being satisfied is causing many potential investors to look elsewhere.

Indeed, over two thirds of those asked (67%) had concerns that the necessary repayments would not be satisfied, with many looking elsewhere for more control over their investment.

Of course, this all comes down to the reliability of the borrower. Where a company is not explicit in what the funds will be used for, or if you are investing in a new company with no experience of repaying loans, the risk is of course higher.

However, making an investment with a borrower that has previously paid back on investments with interest, and given you have done sufficient due diligence on the borrower, you minimise the risk of the repayment not being met. Using an investment company is a common method for investors entering the market.

Debt investment can be low risk if investment companies carry out extensive due diligence. Ensuring that the borrower has the income and assets in place to repay the loan, even if conditions change in the investment, is the vital initial step of due diligence. Past examples of firms not being stringent in the vetting process has contributed to some negative views in the market, however, if the preparation is done right, it can be a safe and highly profitable investment to make.

Two thirds of investors are hesitant of this investment through fears that the borrower will default on the loan. Investors need to be careful about the investment they enter into, and companies should be doing strong due diligence to improve reliability in the market.

If you are interested in making a debt investment, there are a number of companies that specialise in introducing you to suitable investments.

Here at FJP Investment, we monitor trends closely on an on-going basis. We provide detailed insights into the way investors act in the market and how they can plan their investment, and we attempt to understand consumer behaviour in the market.

Due diligence is also a priority here at FJP Investment, we undertake a number of tests to ensure our clients funds will be as secure as possible, including securing the investment against the asset.